Keynote address at ZS Leadership Offsite in Trivandrum, March 13, 2015

Being World Class in India is a very inspiring topic and I thank you for inviting me to share my thoughts on it. This topic is very close to my heart. I have spent the last 13 years living this – 8 years building the McKinsey Knowledge Centre and the last 5 years leading Fidelity’s Offshore operations. I have also had the opportunity of seeing this topic from an industry perspective. I have been involved in setting up the NASSCOM forum for multi-national companies, earlier called Captives, but we now call them GICs (Global In-house Centers); you will hear me use the term GIC a lot in my talk!!

Each GIC believes it’s unique. However, as we brought them together we realized that GICs even those across diverse industries, have so much in common. Most deliver solid value back to their parent enterprises and the stakeholders are very satisfied, but at the same time are also searching for answers on how to raise the game and deliver the next level of value. Over the last 3-4 years we have done a series of research projects to understand what various GICs are doing on value addition and how they can accelerate their value addition journeys.

Today I would like to share with you some insights based on this research work and my personal experiences. Will try to explore the following 5 questions:

- What does being World Class mean for a service organization?

- Why is the World Class journey important?

- What are other service organizations doing?

- What are the key success factors?

- What do leaders need to do differently?

- What does being World Class mean?

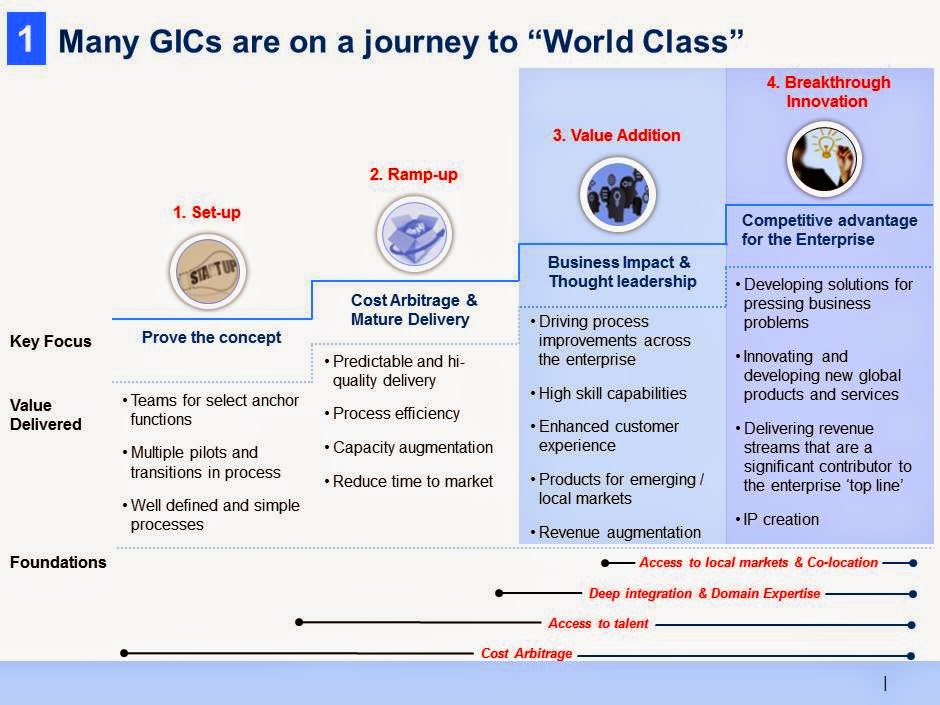

Being World Class is not a destination, it is a journey. What was World Class just a few years back is now business as usual. Just a couple of years back, going beyond scale & delivery and building high-skill capabilities was a big aspiration. Thought leadership and business impact were the key buzz words. Today many GICs are already there or at least attempting to get there.

The new benchmark for World Class for GICs is about breakthrough innovation. This is not just about incremental improvements, but how do you develop IP and new products and services that make a real difference to the company’s top line? How do you transition from being a Cost Center to a Revenue Center? How do you become a solution to the most pressing business problems the enterprise is facing? For example, how do you respond to tectonic shifts like digital disruption that is transforming so many industries?

In summary, for me being World Class is about being the source of competitive advantage, the “secret weapon” for your firm. Many years back in the early stages of my journey at the McKinsey Knowledge Centre, we had set a visual picture for what success should look like. It was that in a few years’ time Harvard Business Review carrying a cover story on what makes McKinsey such a remarkable firm, and that the knowledge center was the secret to its success. That picture might still be a good aspiration for what being World Class means to a GIC!!

- Why is the journey to World Class important?

GICs have quite a unique opportunity to march forward towards being World Class and being the source of breakthrough innovation and competitive advantage for their enterprises. There are multiple factors coming together that make this journey not just feasible but also an imperative.

- GICs have matured and have a great platform to build on. They have built expertise, not just functional and technical knowledge, but domain and business knowledge. In most cases there are strong management teams that have credibility within the global organization. There is deep integration with the parent enterprise that facilitates knowledge transfer. They have built scale and often have multiple functions co-located. This is a huge opportunity for innovation, which is still under-tapped. Access to large customer data sets, which is an interesting opportunity for pattern recognition. And, proximity to local markets provides a great opportunity for building products and services for emerging markets that are so important for many global organizations today.

- That was the supply side, if you look at the demand side businesses are facing unprecedented velocity of change. Core markets are diminishing, new ones are emerging. Customer preferences are changing and customer delight is becoming a bigger imperative than ever before. Then there is the impact on the Technology megatrends – social, mobile, analytics and cloud. Combination of these trends means that traditional business models are getting disrupted and innovation is not a ‘nice to have’ but an imperative. This also means that enterprises are now more open for looking at new sources of innovation (for example the GICs) that might not have been on their radar earlier.

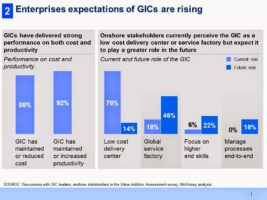

- Combinations of the above demand and supply side factors have resulted in enterprise raising their expectations from the GIC. A survey that McKinsey had done showed that while the current positioning of GICs might be that of delivery centers there is increasing expectation going forward of GICs making more value added contributions

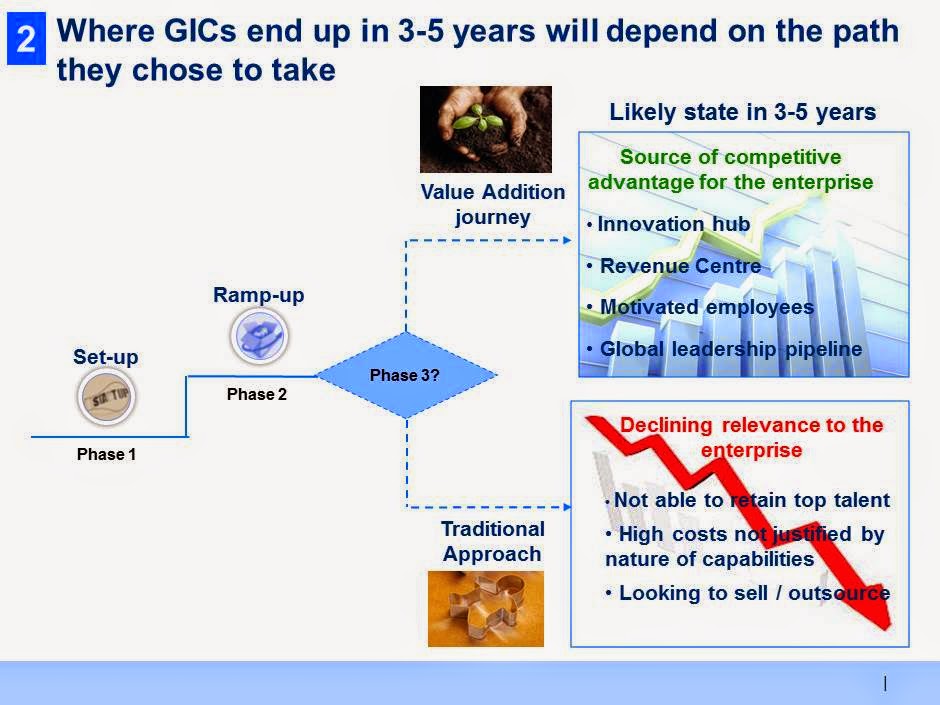

- While we are talking about an upside, there is also a downside that GICs need to be aware off. Being stagnant can be the ‘kiss of death’. With just business as usual, you will lose relevance for the enterprise. Moreover, this is a very dynamic talent market, and thus it will be very difficult for you to retain your best talent. So, there is a fork in the road. If you move up the value addition journey you can create a World Class asset; however, if you stay stagnant, you might face terminal decline. Clearly, value addition for GICs is not just an opportunity but an imperative. Relevance and, in many cases, survival will depend on being able to forge a value addition journey that takes the GIC beyond cost arbitrage and scale & delivery as its raison d’être.

- What are other service organizations doing on value addition?

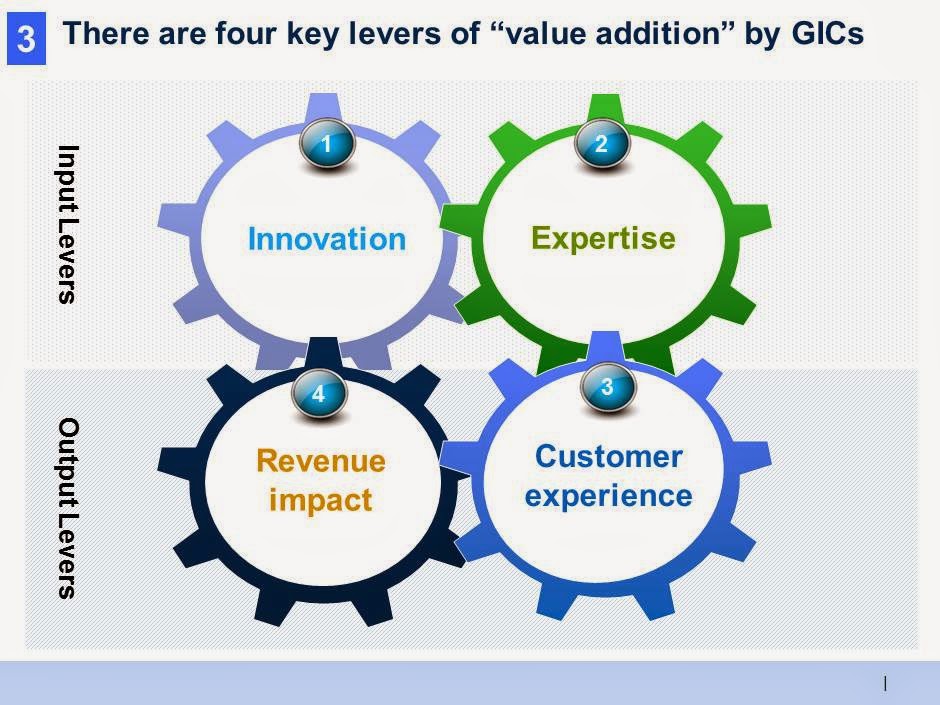

Now that we have looked at the “why’’ of World Class lets go back and look at the ‘’what’’ in more detail. We have spent a lot of time over the past 3-4 years in NASSCOM and surveyed over 50 companies to understand what GICs are doing on value addition, and based on that developed a framework that can be used across the industry.

Our framework for value addition for GICs has 4 interlocking levers – Innovation, Expertise, Customer Experience and Revenue Growth. These are interlocking levers as they all have an impact on each other. I call Innovation and Expertise the input levers and Customer Experience and Revenue impact the output levers from an organization perspective.

- Many GICs started their Value Addition journey by focusing on Expertise. We see many examples: business research, investment research, analytics, R&D and many more. While building these hi-skill capabilities in itself has been a great value-add, they have also helped raise the organization DNA of the GICs. This has helped create more opportunities for innovation and also raise relevance of the GIC for the senior management.

- We have already mentioned Innovation many times. Most GICs have historically had a strong culture of process improvement as transition of work offshore was a natural opportunity to upgrade the processes. GICs are beginning to go beyond process innovation and focus more on product innovation. Tech product companies like Cadence and SAP have been doing some great work on product innovation and there is opportunity for Service companies to learn from them

- In the fiercely competitive business environment we have today, improving customer experience is a key priority. For example, in my firm Fidelity improving our customer Net Promoter Score (NPS) has become one of our foremost KPIs, as or perhaps even more important than asset gathering and profitability. Given the scale of GICs and the fact that they are engaging deeper and deeper into the customer delivery process, GICs have a unique opportunity for raising the bar on customer experience

- Revenue impact is the Holy Grail. Most GICs started as cost centers but there is real opportunity for them to contribute to the top line both directly and indirectly. Analytics has opened up so many avenues for improving marketing effectiveness and therefore revenue yield. What I find very exciting is that many GICs are designing and delivering end-to-end services that have significant revenue impact thus making a direct impact to the top-line.

There is some skepticism on impact GICs can make on Customer Experience and Revenue Growth. To some, these might seem like a bridge too far. I have seen 6 principles to drive end-customer and revenue centric value addition.

- Leverage lower cost to serve to extend coverage of services to segments that are difficult to serve with traditional models. A significantly lower cost structure opens up opportunities that might otherwise be difficult to access. Many banking GICs have used this principle to extend the coverage of Collections services below traditional ticket sizes. Investment banks have also used this principle to extend their stock coverage.

- Source superior talent (given availability of hi-quality talent at low costs) to dramatically raise service quality. Instead of aiming for 5-6X cost arbitrage, some companies go for lower arbitrage and invest the surplus into significantly raising the talent profile relative to what they have worked with in the past. This is huge opportunity to totally redefine service quality. When the McKinsey Knowledge Centre started in 1998, it started by hiring 10 MBAs. This was a significant departure from tradition as McKinsey had until then largely relied on library and information science profiles for its research function. This was a game changer and eventually led to a significant upgradation in the scope and role of research function globally in McKinsey.

- Reduce “hurdle rate” for innovation making possible initiatives that might otherwise be not feasible. Combination of low costs and hi-quality talent is a great enabler for innovation. I call it the “Golden Equation”. Traditionally lower costs have been leveraged for reducing the cost per unit of services. The same can be leveraged to reduce the investment costs for innovations. This can allow an enterprise to de-risk its innovation program and simultaneously increase the innovation capacity significantly. I have leveraged this principle both in McKinsey and Fidelity, where we set up new specialized Analytics services for the firms from India. Setting these new capabilities in New York and London respectively would have been very expensive and thus these ideas might have never seen the light of day. We were able to get going on pilots for these in India with minimal investments and prove the concept. Many companies intuitively leverage this principle. There is a tremendous opportunity to use it more explicitly.

- Leverage customer data to do “pattern recognition” of customer needs to design new/ refined services. Many GICs run customer delivery processes and are therefore close to customer requests and data. This is a tremendous opportunity to not just learn more about customers but to leverage the insights to develop new products to serve repetitive customer needs and solve pain points. At the McKinsey Knowledge Centre we analysed the research requests coming from consulting teams to develop a series of research products that not only raised the analyst productivity but improved the quality significantly. These research products eventually formed the basis for new research oriented services that McKinsey introduced for its clients.

- Leverage co-location of functional and regional capabilities to drive new service models and innovation. Many GICs are a microcosm of their entire firm. They often house multiple functions and serve different business lines and geographies. This co-location is a unique opportunity for collaboration, which might not be available to the firm anywhere else in the world. New, innovative ideas often come not within a box but at the intersection of many boxes. Especially powerful are the collaboration opportunities between Analytics and Technology in the Big Data space and between Operations and Technology given the increasing push towards automation and creating service platforms. Also powerful is the opportunity for knowledge sharing and creating global products/capabilities when functions serving different geographies are co-located.

- Drive product/service innovation for emerging markets. Many enterprises have leveraged their GICs as an incubator for launching their businesses in the local markets. The opportunity goes beyond just rolling out traditional services in these markets. Emerging markets like India are often very competitive and require innovations in service offerings and delivery models to be successful. These innovations in services and products can be powerful exports to more developed markets. McKinsey did some of its most significant experiments in “productizing” its knowledge capabilities into new client service lines in India leveraging its Knowledge Centre. Many of these services eventually developed into large global service lines.

- What are the key success factors?

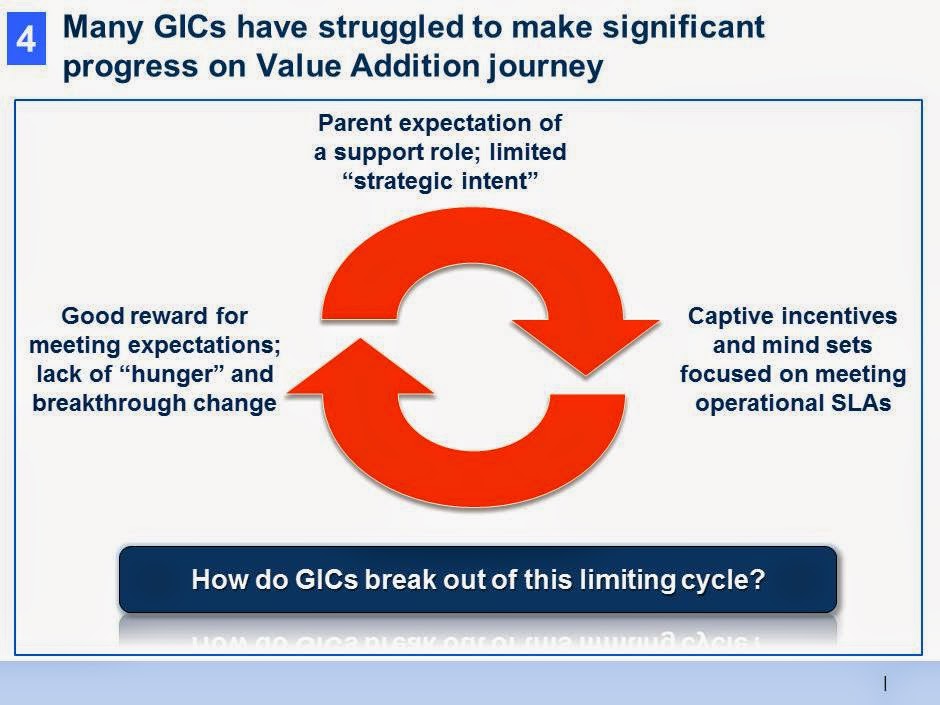

Despite the tremendous potential many GICs have not made as much progress on Value Addition journey as they should have. The key reason why the outcomes have not always lived up to the potential is because many GICs and their managers are trapped in a “comfort zone”. Expectations from onshore stakeholders are sometimes moderate – focused on getting leverage for execution and not thought leadership. The GIC talent is typically hi-quality and are able to deliver on the delivery expectations without much intellectual stretch. And the rewards for the GIC staff are attractive (at least relative to the stretch and risk they are taking!). It ends up being a comfortable, symbiotic relationship that keeps on perpetuating as there is little drive and “hunger” to change the status quo.

However, this comfort zone and the negative cycle it perpetuates is a slow but sure ‘kiss of death’. This “business as usual” cycle slowly dulls the individual capabilities and the organization culture. The outcome is that even when there is an urgent need for the organization to raise its game, the GIC and its managers are not in a position to step up.

It is imperative that GICs make sure that they don’t fall into such a limiting cycle or if they are in one, they break out of it. I believe there are 5 success factors that can help GICs build the culture and capabilities required to accelerate their journey to World Class:

- Shape and align onshore stakeholder expectations. First, engagement is needed with the CEO and business leaders (vs. just the COO/CFO functions in traditional approaches) to ensure that the game changing opportunities that GICs can provide are being considered as part of business strategy discussions. Second, the organization changes required are so significant that it needs global senior management sponsorship. To realize the full potential of the GIC changes are required not just in the GIC but concurrently in the global organization e.g., service strategies, talent models. It often means challenging some of the key design principles and orthodoxies of the global firm. For this to happen, the CEO and senior management need to be involved and understand the GIC more deeply than what they would do typically, and signal their change expectations clearly.In my experience while the senior business leaders might not be close to the GIC, with the right set of facts it is not difficult to get them excited about the business opportunity. The bigger challenge of changing expectations is often with the middle managers, who are less directly responsible for business outcomes. They are often more vested in legacy operating models, have greater need for control, and are thus less change ready. Therefore, it is important to develop a network of business zealots who will become internal promoters and champion the value addition journey of the GIC. It might also mean that you focus on pilots where you demonstrate the much higher level of value add instead of trying to raise the game across the board.

- Develop governance model that balances global integration and local autonomy. Both the commonly seen governance models i.e., “shared services” and “vertically integrated,” are inadequate. A shared services model is efficient but does not generate stakeholder ownership, while vertically integrated models ensure stakeholder ownership and knowledge transfer but tend to encourage the status quo. To drive innovation and higher levels of value addition, you need both global, functional integration and strong local leadership that can identify and drive opportunities. There is often tension between these two axes of the matrix. Senior management needs to be aware of this tension and help find the right balance.In addition, GIC leaders should be senior enough so they have a “seat at the table” and are empowered to drive significant initiatives and decisions. Often this might require going beyond traditional organization structures and hierarchy.

- Build management practices for deepening business knowledge and innovation. Value addition and the journey to World Class is not an accident, you need to consciously invest in the right management practices. A key requirement of the value addition journey to world class is to build deep business knowledge and intimate understanding of customers and their pain points. Traditional training and development structures that GICs are typically good at might be less helpful here as they are for strengthening technical and process knowledge. Investing in travel and global rotations might have higher impact. Many GICs bring in expat managers for functional expertise. However, it is even more important to bring in senior professionals from the business side of the organisation. Such moves might be difficult to pull off but if done well can help connect GIC deeply into the business.Many GICs have strong programs for process improvement. However, they need to build stronger processes for nurturing innovation. Enterprises should consider having an explicit budget to fund innovations in their GICs. It can have a big pay-off relative to the size of the investment.

- Embedding a risk-taking and entrepreneurial culture and nurturing managers to step-up as global, thought leaders. To institutionalize the ongoing journey to world class it is important to build a culture of excellence that encourages risk-taking and entrepreneurial behaviours. Organization’s culture has a recursive relationship with its leaders. It influences the behaviour of the leaders but is equally shaped by them. In GICs we typically have hi-quality, effective managers. However, there is need from them to raise their game and step up as leaders. I will talk more in the next section the shift managers need to make. From an organization perspective it has three important implications: 1) Redesign current leadership development frameworks and approaches to focus on entrepreneurial behaviours and thought leadership. 2) Might need to supplement current management teams by getting hi-quality talent from outside. 3) Embed the new leadership expectations into the performance management systems. In many cases, GICs focus on tenure and performance in current job for promoting their managers. They might need to change emphasis to assessing potential (and not just performance) and have stronger focus on hi-potential talent cutting across tenure and levels.

- Learn and collaborate with the local ecosystem. We are fortunate to be in one of the most well-developed and active industry ecosystems in the world. We have GICS, Indian IT/BPO companies and Product Start-up co-existing. There are opportunities for GICs to learn and collaborate across all 3 types of players.Sharing best practices and success stories can help GICs learn from each other and get both ideas and motivation to move to the next level. Joint problem solving on common topics through GIC forums can yield insights that companies might struggle to reach individually. This industry discourse and collaboration can help raise the bar for the entire industry.“Make vs. Buy” has been a perennial debate. Many organizations have now moved beyond this debate and recognized that there is a role for both and these models can co-exist. Therefore, hybrid sourcing is now increasingly becoming the norm with GICs often playing a key role in managing the partner relationships. This provides a great opportunity for the GIC to work closely with IT/BPO vendors and learn from them where it makes sense.One of the most interesting collaboration opportunities today for GICs is leveraging the product start-up ecosystem in India. There is tremendous change happening in the technology space and it is not possible for anyone organization to be at the cutting edge of all of it. Especially for the more traditional organization making the transition to a digital enterprise can be highly challenging. In response, many GICs have set up incubators (e.g., Target, Pitney Bowes) to work closely with tech start-ups. This and other modes of collaboration with start-ups can be a very interesting option for GICs.

What do leaders need to do differently?

My most important message is for all of you, the leaders in the room. Marshall Goldsmith’s famous call, “what got here won’t get you there” rings so true for us. ZS is a successful organization in India and so is the case for most GICs in India. To deliver on the execution oriented expectations required a certain type of mind-sets and capabilities. To deliver on thought leadership and innovation required to be world class calls for different mind-sets and capabilities. Therefore GIC leaders need to make 4 important shifts:

- From Operations Managers to Thought Leaders & Innovators. Our managers are very good at execution and getting things done, whether project delivery or managing service quality. To be a thought leader and innovator they will need to build strategy and critical problem solving skills. They will need to change their mind-set from focusing on the Urgent and the near-term to learning to deal with the Important but Not-Urgent, because that is the nature of lot of thought leadership and innovation. They will also need to need to manage more complex conversations. Managing execution involves relatively structured and predictable conversations. Thought leadership will be more complex conversations and more possibility for conflict with onshore stakeholders who might not be used to that mode of engagement back from the Offshore managers.

- From Functional Experts to Business Experts. We have strong technical and process skills; however, the key success factor in the next stage of the value addition journey is business and customer knowledge. Managers will need to invest in this self-learning or they will get left behind.

- From “Safe pair of hands” to Entrepreneurial Risk Takers. Our current processes and delivery models are often designed to minimize risk and ensure predictable delivery. For this we have tended to look for and encourage “safe pair of hands”. In an era where innovation is paramount, you need entrepreneurial risk takers. This is not a simple change as it is deep rooted in the culture of the organization. Senior most leaders have to personally signal the culture change through their own actions.

- From Local Champions to Global Influencers. From managing teams locally increasingly the expectations will be to lead and influence globally. This requires high levels of multi-cultural sensitivity, sophisticated communication skills and most importantly deep understanding of global organization priorities.

In summary, the change is for our Managers to step up to being Leaders. The most critical aspect in this change will be drive, “hunger” and a relentless pursuit of excellence. If we can build and sustain that passion and energy, rest of the changes will follow.

To conclude, GICs are at a very exciting juncture. There is strong momentum and a real opportunity for them to move to a next level in their journey to World Class, where they become a source of competitive advantage for their global organizations. I hope this note provides GIC leaders with some good ideas and inspiration to realize this wonderful future for their organizations and for themselves. It will not be an exaggeration to say that the future of GICs depends to a large extent on how the GIC leaders step up and drive change. So my message to all the GIC leaders is “Carpe Diem” – seize the day!!